Anthropic overtook OpenAI to reach a 1 trillion valuation-open the list of investors/It has to do much more than selling models

In March, OpenAI received $122 billion in funding round /valuation of $852 billion. On May 28, Anthropic Series H received US$65 billion/post-investment valuation of US$965 billion/overtook OpenAI for the first time/nearly US$1 trillion. A year ago, Anthropic's annual revenue was 10 billion yuan/this round announced a run rate of 47 billion yuan/ 12 months, up 4.7 times. The market explanation is consistent- Claude Code sells well + the business model works well. But I opened the list of investors and saw a few things that were not mentioned much in other articles- Samsung / SK Hynix / Micron three memory chips were simultaneously listed as strategic investors + signed a seven-year, US$1.8 billion edge cloud agreement with Akamai on the same day + the Mythos model is about to be opened (with the ability to find vulnerabilities + chain attacks)+ the investor structure is all stable old money (Sequoia / Capital Group / Fidelity / GIC, etc.)/There is no typical AI hot money. Together- Anthropic is building the next generation enterprise + government AI infrastructure stack/on the same level as 1990s IBM, 2000s Oracle and 2010s Microsoft.

On May 28, two news items in overseas AI circles collided.

One is Anthropic announced the completion of Series H financing-a $65 billion sum/post-investment valuation at $965 billion/nearly one trillion. For the first time, this figure exceeded OpenAI's $852 billion valuation after its March round of $122 billion funding. The valuations of the two companies with the most aggressive big models have reversed.

Another article/On the same day, Anthropic released the Claude Opus 4.8 model/released an agent orchestration tool called Dynamic Workflows/also demonstrated that Claude Code can run hundreds of thousands of lines of code end-to-end large-scale migration. Only 41 days have passed since the previous version of Opus 4.7- Anthropic used it for more than half a year from Opus 4.0 to 4.7. The rhythm is obviously pressing.

Two news pieces put together/The entire overseas technology community has been discussing the same thing this week--

Why did Anthropic surpass its valuation?

The discussion concluded almost unanimously. Claude Code sold out/A CLI tool supported a company/enterprise developer market and was captured by Anthropic.

This explanation does sound enough. A year ago, Anthropic's annual revenue was US$10 billion. This round announced that the run rate has reached US$47 billion/ 12 months, a 4.7-fold increase-this is the strongest growth curve in the entire AI industry in the past 18 months. Combined with Claude Code's reputation in the developer circle/the explanation of "selling + running through"/it seems to be a closed loop of logic.

But I repeatedly read this round of financing announcements/corrected the list of investors one by one/found something that other articles did not mention much--

What Anthropic is doing is much bigger than just "selling models."

If you understand this matter clearly, you will re-understand why the figure of 965 billion is beginning to make sense. We will also re-understand/why/starting from the second half of this year/the entire enterprise IT industry will be shuffled again.

{kind=link}

QKPFX0 The first surprise on the QK investor list

Let's start with who will pay for this round of US$65 billion.

There are four leading investors- Altimeter Capital (Brad Gerstner's hedge fund)/ Dragoneer / Greenoaks Capital / Sequoia Capital. According to people familiar with the matter, each family invested more than US$2 billion in this round/add up to US$8 billion in the lead.

There are 6 joint investors- Capital Group (veteran US mutual fund manager/manages US$2 trillion in assets)/ Coatue Management / D1 Capital Partners / GIC (Singapore sovereign wealth fund)/ ICONIQ Capital / XN.

The institutions/names that follow the investment are not unfamiliar- Baillie Gifford (Scotland's Centenary Asset Management/used to be a major shareholder of Tesla / Amazon)/ Blackstone/ Brookfield / D.E. Shaw Ventures / DST Global / Fidelity Management & Research。

Add up these names/you will find one thing--

All are veteran Wall Street asset management + veteran sovereign funds + veteran private equity.

There is no SoftBank. No Tiger Global. There is no typical "AI hot money" fund. There is also no growth fund that usually spends money in Silicon Valley and specializes in chasing growth stories.

Compare OpenAI's core investors in the past two years-MGX (United Arab Emirates Sovereign AI Fund/specially established for AI)/ SoftBank / Microsoft / Khosla Ventures /and a series of Silicon Valley growth funds.

OpenAI's list is a structure of "sovereign hot money + strategic giant companies + growth funds". Anthropic's list is a structure of "stable old money + long-term asset management + sovereign allocation".

These two structures correspond to two completely different types of companies in the secondary market.

The first structure corresponds to the consumer Internet leader-high valuation/high imagination/emphasis on growth/no emphasis on short-term cash flow. Meta / Snap / Pinterest /early Uber /are all this way.

The second structure corresponds to corporate infrastructure giants-stable valuations/long contracts/renewal rates/cash flow predictability. Oracle / Salesforce / ServiceNow / Palantir /are all this way.

Funds will choose targets that match their investment logic. Anthropic's list is telling you-- ** Its funding side is pricing it as an "enterprise infrastructure giant"/not a "consumer Internet leader."**

This was the first accident. But not the most unexpected.

Second Accident/On the List of Strategic Investors

This round of lead + follow-up investors/ Anthropic itself disclosed the list of "strategic infrastructure partners"-strategic infrastructure partners.

3 names--

Samsung。SK Hynix。Micron。

Three companies making memory chips/strategic investors who joined Anthropic at the same time.

This matter has no precedent in the AI industry in the past five years.

The strategic investors of a general AI model company cannot fall into three categories-cloud manufacturers (Microsoft / Amazon / Google / Oracle)/key customers (Stripe / Notion / Salesforce)/chip heads (Nvidia /occasionally AMD).

Samsung / SK Hynix / Micron are doing DRAM / HBM high-bandwidth memory/ NAND flash memory. This is the "blood" of AI reasoning and training-model weights must be placed in HBM/ KV cache must be swiped repeatedly in memory/long contexts must be called in memory. But what they do is not something related to "direct sales models".

Three companies entering the Anthropic Strategy at the same time can only mean one thing--

Anthropic is holding something completely different from "selling models."

The relationship between this matter and memory chips will be clear in the next section.

also signed another US$1.8 billion contract on the same day as May 28

Opus 4.8 released + Series H closed + and third thing/ 5/28 same day--

Anthropic signed a seven-year,$1.8 billion cloud deal with Akamai Technologies.

Akamai may not be familiar with this company/domestic readers. It was a CDN (Content Delivery Network) veteran/founder that emerged from MIT in the late 1990s. Daniel Lewin died on a plane on 9/11/was the first victim of the attack.

Akamai is different from mainstream clouds like AWS / Microsoft Azure / Google Cloud-its servers are distributed on edge nodes in 4200+ cities around the world/rather than concentrated in a few very large data centers. Each node is only 1-2 hops away from the end user.

For the past 25 years, Akamai's main business has been "videos you watch/web pages you load/games you play/closer to you."

Anthropic's $1.8 billion sum is asking Akamai to do a specific thing--

Let Claude run on the edge/not just run on the central cloud.

Why would you do this?/ Anthropic itself gave a number in its announcement-its API usage has increased about 80 times in the past year.

What is the concept of 80 times?

If Anthropic handled 100 million API calls per day a year ago/it is now 8 billion. On average, each call requires reading thousands of tokens of context/calculating thousands of tokens of output/checking KV cache /pull model weights in the middle.

This magnitude/all follows central cloud reasoning-the latency is too high (users need to wait a few seconds between entering and AI responses)/the cost is too expensive (rent is rising for each H100 GPU)/the bandwidth is unaffordable (data center outlet traffic explodes the meter).

If you want to continue scale / Anthropic, you can only go in one direction-reasoning sinks.

Inference sinking means-don't let user requests travel all the way to AWS rooms in California/Instead, run part of the model on nodes closer to the user. Users in Tokyo/Run Claude on Tokyo Edge nodes. Users in Frankfurt/Running on German edge nodes. This reduces the latency from a few hundred milliseconds to tens of milliseconds/the outlet bandwidth pressure is dispersed/the user experience is much better.

This is "marginal reasoning".

What does marginal reasoning need?

First, we need edge servers all over the world-this is the 4200+ nodes provided by Akamai.

Second, you need to have enough computing power + memory + storage on each node-this is what the three memory chip companies Samsung / SK Hynix / Micron can provide.

The characteristics of edge nodes are that it is impossible to house a cabinet of GPUs (too expensive and too hot)/the memory bandwidth of each chip must be efficiently utilized. Samsung's HBM4/ SK Hynix's next-gen HBM / Micron's LPDDR5X-these products determine where the bottleneck for marginal reasoning lies.

So you look back--

It is no coincidence that Samsung + SK Hynix + Micron entered strategic investments on the investor list.

A US$1.8 billion seven-year contract with Akamai/No coincidence.

These two things are two actions on the same strategic path--

Anthropic holds the next generation AI computing stack. This stack will not all run on the central cloud-it will be distributed across the central cloud + edge nodes + user equipment levels. If this matter goes through/ Anthropic is no longer just a "model company"-it is an "AI computing stack infrastructure provider."

This is a much larger location than OpenAI's "selling ChatGPT subscriptions".

{kind=link}

The third thing/Mythos that has not yet been officially released

The same day that Opus 4.8 was released/ Anthropic slipped a sentence in the announcement--

"Our Mythos-class model/is about to be open to all customers. just a few weeks。」

What is Mythos?

Anthropic gave a tentational preview before. The preview was stopped within a few days at the time-citing "raised cybersecurity concerns"/raising cybersecurity concerns.

Then what exactly can this model do/ Anthropic himself clearly described it in the announcement--

Mythos「has the ability to find vulnerabilities in existing software and chain these vulnerabilities together to execute sophisticated cyber attacks」。

Translation- Mythos can scan existing software/find vulnerabilities/chain these vulnerabilities/perform complex cyber attacks.

This is a model of capable red team + penetration testing + vulnerability exploitation chain generation.

In the network security industry, this capability is called "offensive cyber capabilities"-offensive cyber capabilities. In the past, only a few national-level APT teams and top commercial security companies (Mandiant / CrowdStrike) had this capability.

Normal AI companies/This ability will not proactively open up.

Think about what would happen if OpenAI opened up similar capabilities-the next day there would be prompt injection to ask ChatGPT to help you generate phishing emails/the third day someone used it to attack the U.S. power grid/the fourth day Sam Altman appeared at a congressional hearing.

Anthropic is ready to go. The original words are "coming weeks."

Why does it dare to release it?

There are two levels of speculation--

The first level- Anthropic's entire brand positioning is "safety + alignment + responsible scaling". It will split from OpenAI in 2021/The core narrative of the brothers and sisters Dario Amodei + Daniela Amodei is "We make the safest AI possible." This brand asset means- Anthropic's ability to release cyber/supervision will be more tolerant/customers will trust them more. The same ability is in the hands of OpenAI/ Sam Altman will tweet and apologize the same day. This is brand moat.

The second level- Anthropic is likely to be seizing a market that other AI companies dare not enter. This market is--

** Government + Defense + Critical Infrastructure Defense + Internal Security of Large Enterprises. **

The customers of this line are-the U.S. Department of Defense/NSA/ CIA /banks/power grid companies/large manufacturers. The money they spend on cybersecurity every year-more than $200 billion globally-has been growing at 12-15%.

Who was the biggest player on this line in the past? Palantir。Palantir now has a market value of about US$400 billion (as of early 2026)/It relies mainly on long-term contracts in government + defense + key industries.

If Anthropic enters even 20% of this market through the Mythos + Claude package, it will be US$40 billion per year in long-term contracts-a high-profit long-term contract business that OpenAI's "ChatGPT subscription" model will never be able to achieve.

Mythos launches- Anthropic enters a market that other big model companies dare not enter. This is another brand new puzzle.

puts these 3 things together

Now let's put together these three events at Anthropic's end of May--

In the first item/investor list, three memory chips, Samsung + SK Hynix + Micron, have simultaneously made strategic investments.

The second one/signed a seven-year, US$1.8 billion edge cloud agreement with Akamai/pledged a generation of distributed AI inference infrastructure.

The third thing/Mythos model will soon be opened/ cyber capabilities/Seize government + defense + key industry markets.

Every single item is/an independent industry news piece this week/it won't make people feel that great.

Put it together--

**Anthropic is doing much more than selling models. **

It is building something-the next generation enterprise + government AI infrastructure stack.

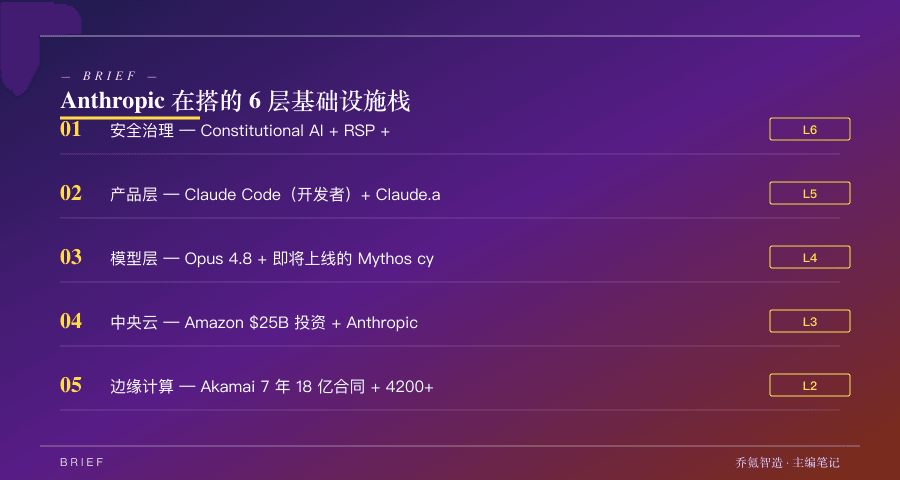

The complete stack looks like this--

The lowest level/is chip + storage cooperation (Samsung / SK Hynix / Micron strategic investment/getting priority supply of the next generation HBM + LPDDR).

Further up/is compute distribution (Akamai's $1.8 billion 7-year contract/ 4200+ edge nodes/reasoning sinks to the closest place to the user).

Further up/is a major sovereign cloud company (Amazon invests $25B/ Anthropic promises $100B to AWS a 10-year contract/locks in the central cloud's super computing power).

Further up/is the model level (Opus 4.8 + upcoming Mythos /Covering General Reasoning + Programming + Cybersecurity).

Further up/is the product level (Claude Code as the developer portal + Claude.ai as the enterprise knowledge work portal).

The top level/is security + governance (Anthropic's entire brand assets + Constitutional AI methodology + RSP framework).

Add these 6 layers together- Anthropic doesn't sell API calls. It sells--

**"Enterprise AI brain"+ deployment capabilities + computing power support + security + governance framework package. **

You are a major U.S. bank/want to connect the entire company to AI - Anthropic can cover you up/you don't have to sign up 10 more suppliers.

You are a state government/want to use AI to automate benefit reviews-the Anthropic family can go from model to deployment to compliance.

You are a big manufacturer/want to do Industrial AI -the Anthropic family can give you the full stack from the edge to the cloud.

This size has exceeded the scope of a SaaS company. The benchmark is the position of corporate infrastructure giants--

IBM was in this position in the 1990s-it didn't just sell hardware/it sold "total enterprise computing solutions." Every Fortune 500 company is a long-term contract customer of IBM/one contract lasts for 10 to 20 years. At its peak in the 1990s, IBM's market value reached as high as US$200 billion-which translates to today's purchasing power of approximately US$500 - 600 billion.

Oracle was in this position in the 2000s-it sold enterprise databases/but essentially sold "enterprise data infrastructure." Larry Ellison single-handedly made Oracle a supplier that the IT departments of large enterprises around the world cannot avoid. Now it has a market value of about US$1.5 trillion.

Microsoft was in this position at the time of its cloud transformation in the 2010s-Microsoft had a market value of $300 billion when Satya Nadella took over/repositioned itself as an "enterprise cloud infrastructure" through Azure/now has a market value of $3.5 trillion.

What Anthropic wants to be in this position in the 2020s- ** corporate + government AI infrastructure giant **.

The valuation of US$965 billion is reasonable when placed in this benchmark. It's not competing with OpenAI on "how many ChatGPT subscriptions will be in the next month"-it's competing with Microsoft / Oracle / Palantir for the "next generation enterprise IT infrastructure" position.

The ## investor structure actually confirms this matter

Now look back at the list of "stable old money"/you will find that the logic of the capital side also matches--

Sequoia / Capital Group / Fidelity / GIC / Baillie Gifford / Blackstone / Brookfield --

These funds manage pensions/sovereign wealth/long-term family offices. Their preferences are--

Long cycle. Predictable cash flow. Huge enterprise-level business. Low volatility. 20-30 years can be seen clearly.

They buy Anthropic /are buying the status of "Enterprise AI Infrastructure Leader in the Next 10-15 Years".

They're looking at--

How many long-term contracts with Global 5000 companies can Anthropic sign? How many government take-or-pay agreements you can get. How many countries can I obtain the qualification of a critical infrastructure supplier? Can it stabilize the annual growth of 30-40% /maintain the gross profit margin above 70% after the IPO?

What they are looking at is not-"How many daily activities will ChatGPT product have next month","Will Sora's next video flash","Can o4 rank first in mathematics evaluation?"

OpenAI's MGX + SoftBank + Khosla structure is betting on "consumption + growth + imagination + event-driven valuation."

Two bets. Two corporate forms. Two exit paths.

On May 28, this sum/surpassed OpenAI in valuation/essentially-

** The first centralized vote for AI industry funds-the "Enterprise Infrastructure Route" won the "Consumption Growth Route". **

{kind=link}

China side/The same thing happened in the same week

The above is about overseas. Looking back at China/the last two weeks of May/the domestic big model companies are actually doing the same kind of action-and they are also building their own version of the enterprise AI infrastructure stack "-with different paths/but in the same direction.

DeepSeek--Today, May 31st/The price of V4-Pro API will be permanently reduced to 1/4 of the original price/input cache hits 0.025 yuan/million tokens /input misses 3 yuan/output 6 yuan. This price is basically the lowest among the global model APIs. During the same period, RMB 70 billion in financing was coming to an end/pre-investment valuation was US$45 billion/setting a record for the first round of financing in the history of China's AI model. Liang Wenfeng publicly promised to continue to be open source/The company's main goal is to "promote the technological boundary/not realize it as soon as possible." DeepSeek's bet is-"extremely cheap open source base + strong engineering genes"/use price to pull the entire market towards itself.

** Ali ** -- 5/20 Yunqi Conference issued Qwen3.7-Max at one time (Flagship model/demonstration independently optimized 1158 tool calls within 35 hours on an unseen chip and achieved 10x acceleration)+ Qianwen Cloud Platform (Aggregating 150+ model APIs such as Qwen + DeepSeek + Kimi)+ Self-developed T-Head ZW-M890 PPU chip + Panjiu AL128 rack-scale server (128 M890 interconnected)-the complete "AI factory" end-to-end stack. In the first five months, Alibaba Cloud's MaaS Token revenue increased 15 times/ AI services totaled 30 billion yuan annually. Ali is building a "full-stack integrated enterprise AI infrastructure"/the China company closest to Anthropic's thinking.

** Byte ** -- 5/28 Volcano Engine Push Agent Plan /Aggregate Doubao-Seed /Seed/Seed Dream + GLM-5.1 + Kimi-K2.6 and other models. Superimposed Douyin/Today's headlines data flywheel + complete cloud infrastructure. Bytepath is the trinity of "content ecosystem + big model + agent platform"-feeding back model + agent with your own content scenarios.

** Smart Spectrum ** -- 5/28 Launched GLM-5.1 High-speed API /Output speed 400 Tokens/s /Complex web page code generation is completed in 30 seconds/ Agent Swarm can instantly dispatch 50 different personalities to answer in parallel. Smart Spectrum is betting on "Speed + Agent Scheduling"/in the same direction as Anthropic Dynamic Workflows.

** Tencent Hunyuan ** --May, open source new generation translation model Hy-MT2 (1.8B /7B/30B-A3B three size)/supports mutual translation in 33 languages + 5 Chinese/dialects. Tencent's path is biased towards "deepening specific categories + WeChat ecosystem linkage."

Together, these five companies have basically formed five enterprise AI infrastructure paths in China: "full-stack school/extreme price school/content ecology school/speed agent school/vertical type deep cultivation school."

Who can get out/We will see in the next 12 months.

Judging from the current form/Ali and Byte are the most promising-because they have a complete end-to-end stack of "home cloud + home model + home chip + home product portal + home application scenarios"/This is the same thing in nature as the stack built by Anthropic through Akamai + Amazon + Samsung. DeepSeek model capacity + high price/but lack of ecology. There is one piece for Zhipu + Tencent Mixed Essence.

Whether China's version of the "AI infrastructure giant" can finally take shape in 12-24 months-this is the most important attraction for China's AI industry in the next year.

QKPFX7 What does QK mean to ordinary people

Speaking of this/you may ask-no matter how high the valuation of these companies is/what does it have to do with me?

It's a big deal. I list three specific things--

** First thing/The company you work for will change. **

If you work in a large company (whether Chinese or foreign), there is a high probability that you will sign a long contract from an "enterprise AI infrastructure giant" within 12-18 months. The high probability overseas is one of Anthropic / Microsoft (bundled OpenAI subcontract)/ Google / Oracle. The domestic high probability is one of Ali/Byte/ DeepSeek.

This matter is directly related to your specific workflow-your daily internal system/internal knowledge base/internal collaboration tools/ Slack instant messaging/Salesforce-like CRM -will be connected to this "enterprise AI brain" within 12 months.

Every weekly newspaper you write. Every email you send to a client. Every plan you make. Every judgment you make in internal discussions.

will be seen/organized/learned by this AI brain.

On the bright side-your repetitive labor will be eaten up. Organize meeting minutes/translate contracts/prepare reports/check internal company information-these things no longer need to be done by you.

The bad side-your output will be continuously measured. Which employee output is really valuable/which is aquatic activity-the AI brain will see more clearly than your immediate boss.

This is happening. It won't wait until 5 years/ 12 months later.

** Second thing/If you are considering buying shares in AI companies. **

The Anthropic IPO time window has been revealed-October-November 2026. OpenAI is also counting down to its IPO. Forge Global reported that two roadshows likely to collide into the same window.

This is the fiercest IPO window in the technology industry since the Netscape IPO in 1995-the year that Netscape IPO launched the first wave of the Internet bubble. There is a high probability that Anthropic and OpenAI will launch an AI bubble.

But be careful-valuation of $965 billion/ run rate of $47 billion/valuation divided by revenue multiple = more than 20 times. The valuation of the top/leading company of the Internet bubble from 1995 to 2000 divided by the revenue multiple/peak period was 30-40 times. Anthropic's current position/is close to the valuation level at the top of the bubble.

That doesn't mean Anthropic will fall-it is supported by a 4.7-fold revenue growth. But $965 billion has priced into the script of "becoming a leader in enterprise AI infrastructure in the next 10 years." The script has to be completed/to support this valuation.

If you plan to buy on the day of the IPO-think clearly whether you are buying in the future or taking over.

** Third thing/Your career needs to be re-planned. **

This is the longest of the five things.

After the enterprise AI infrastructure is rolled out/the demand for middle management positions will first decrease. What the AI brain can do-information aggregation/reporting/cross-department coordination/task dispatch/progress tracking-these used to be core values of middle managers.

In turn, the demand for both types of jobs will increase--

One category is a senior professional position that "can collaborate with the AI brain + point the AI brain + verify AI output"-senior engineer/senior product/senior researcher/senior lawyer/senior doctor.

The other category is "physical world work that the AI brain cannot reach"-advanced nursing/maintenance/decoration/coaching/personal services.

The middle layer-ordinary white-collar/middle management/standardized clerical-will be compressed.

The timetable for this matter is about 24-36 months to show clear signals.

If you're at the middle level right now-use the next 12 months to figure out where you want to go.

Last

Anthropic's US$65 billion payment on May 28/on the surface is "AI company's valuation reaches a new high"/is not fundamentally different from the 20 billion/50 billion/80 billion financing rounds in the past two years.

Dig down one level-it's "Claude Code's business model has worked."

Dig deeper/read the investor list + Akamai contract + Mythos is about to go online together these three things--yes--

**Anthropic is competing for the position of an enterprise + government infrastructure giant/The benchmark is 1990s IBM and 2000s Oracle and 2010s Microsoft. **

The last thing to be remembered in this wave of AI revolution will not be which company has the highest valuation-valuations will change/$965 billion may also become $500 billion in 12 months.

What will be remembered is--

** Someone is building the AI brain + infrastructure that all large companies + all government agencies will need in the next 10-15 years. **

There is Anthropic's "Enterprise Infrastructure" route overseas. OpenAI is betting on the "consumption + growth" route. Microsoft / Amazon / Google are playing their own cards. Palantir is guarding its government market territory.

In China, there is Ali's "full-stack integration" route. Bytebet's "content ecosystem + agent platform" route. DeepSeek is betting on the "extreme price + open source base" route. Intelligence + Tencent + Intelligence + Dark Side of the Moon are running each other.

This race/lasted 18 months. It will enter the finals in the second half of this year.

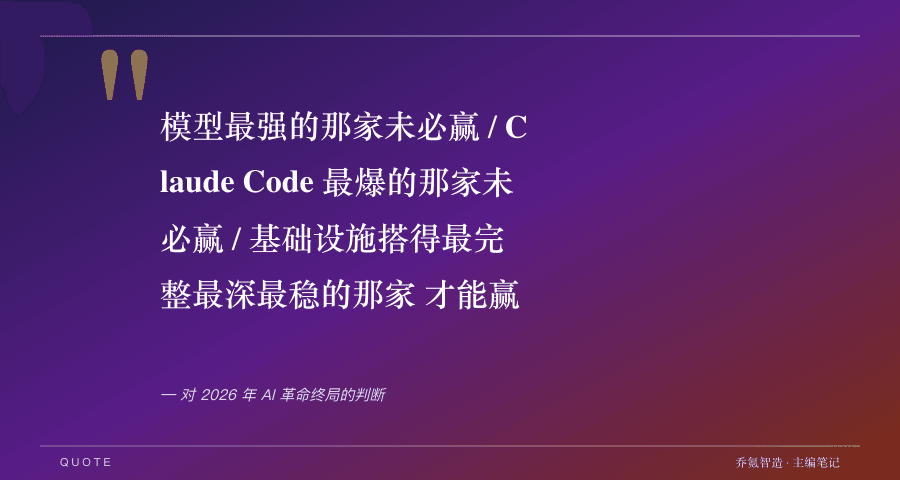

Whoever has the most complete contracts/who can sign the most long contracts/who can live to the market test five years after the IPO +-whoever is the biggest winner of this wave of AI revolution.

The one with the strongest model may not win. Claude Code's most popular company may not win.

The one with the most complete, deepest and stable infrastructure-can win.